🇬🇧 Limited Liabilty Partnership LLP 🇬🇧

What Is an LLP (Limited Liability Partnership)?

An LLP is a hybrid legal structure that combines the benefits of a partnership with those of a limited liability company. Introduced in the United Kingdom in 2001 under the Limited Liability Partnerships Act, an LLP has its own legal personality and offers limited liability to its members, while maintaining management flexibility similar to that of a traditional partnership.

The members of an LLP can be either individuals or legal entities (such as other companies), including non-UK resident foreign entities. This makes it an extremely versatile structure, suitable for international businesses, holding companies, investment funds, professional firms, and digital enterprises with a global presence.

In Northern Ireland, the LLP is governed by the same legislation as the rest of the UK, but may benefit from specific operational advantages due to its strategic position between the EU and the UK.

The Birth of the LLP as a Corporate Structure

The Limited Liability Partnership (LLP) was introduced in the United Kingdom with the Limited Liability Partnerships Act 2000, which came into force on April 6, 2001.

However, this was not merely a theoretical or academic reform: the LLP was created under direct pressure from major professional firms, particularly the so-called Big Four — KPMG, PwC (PricewaterhouseCoopers), Ernst & Young, and Deloitte — as well as prominent London law firms.

These organizations, until then established as general partnerships, were exposed to significant legal and financial risk. Under the traditional English partnership model (regulated by the Partnership Act 1890), each partner is jointly and severally liable for the actions of the others.

In practice, if one partner committed a professional error, all partners could be sued and held personally liable, potentially jeopardizing their private assets.

Limited Liability Partnership (LLP)

The LLP structure was shaped at the request of the Big Four, with a clear objective: to preserve the collaborative nature of a partnership while legally separating the identity of the entity from that of its members, by introducing limited liability.

With an LLP:

The company becomes a separate legal entity

Members are not personally liable for the actions or omissions of others

In the case of professional error, only the LLP is held liable, not the individual members (except in cases of fraud or gross misconduct)

Every risk is contained and quantifiable, making it ideal for large organizations with thousands of collaborators

A Legal Structure Tailored for Modern Risk

In short, the LLP was born out of a concrete and urgent need within the global professional world—to prevent an isolated technical error from destroying the careers and personal assets of uninvolved partners.

Today, thanks to that reform, all of the Big Four operate in the United Kingdom as LLPs, as do the majority of major international law firms, private investment funds, consulting firms, and highly specialized legal boutiques.

The LLP has become the preferred structure for those managing high professional and reputational risk, while preserving confidentiality, autonomy, and contractual flexibility.

Legal Structure with Limited Liability and Efficient Taxation

The Limited Liability Partnership (LLP) established in the United Kingdom or Northern Ireland is an extremely flexible and advantageous business structure, designed to provide legal protection, limited liability, and optimized tax management for its members.

🔒 Limited Liability and Partner Protection

All members of an LLP—whether individuals or legal entities—benefit from limited liability: they are not personally liable for the company’s debts or obligations, except in exceptional cases (such as fraud or serious legal violations).

The financial risk is therefore limited to the capital contributed or held within the LLP.

⚖️ Separate Legal Personality

The LLP is a legal entity distinct from its members. This means it can act, enter into contracts, and assume obligations in its own name, offering further legal protection to the members in case of disputes or creditors.

👥 Company Composition

The law requires a minimum of two members, who may be legal entities (e.g., LTDs, foundations, trusts, offshore companies) or individuals.

There is no maximum number of members, and none are required to be UK residents.

It is also possible to form an LLP composed entirely of non-resident members.

💰 Transparent and Advantageous Taxation

One of the key features of the LLP is its “tax transparent” status:

The LLP does not pay taxes in the UK, unless it operates physically within the territory (e.g., with offices or UK-based clients).

Profits are taxed directly in the hands of the members, in their country of tax residence.

If the LLP has no operations in the UK and all its members are non-UK residents, no tax is due in the United Kingdom.

This makes the LLP an extremely tax-efficient structure, especially when members reside in low-tax or zero-tax jurisdictions.

🌍 When the LLP Is Tax-Neutral in the UK

No UK taxation is triggered if the following three conditions are met:

The LLP has no operational base and no clients in the UK

All members are non-UK residents

The business is conducted entirely remotely or abroad

In such cases, taxation occurs only in the members’ countries of residence, according to local laws.

The Limited Liability Partnership (LLP) is an extremely versatile structure, suitable for a wide range of activities, both in the digital world and traditional commerce.

Below is an overview of the activities that can be legally carried out through an LLP, without taxation in the United Kingdom, provided that the business has no effective base in the UK and the members are non-residents.

Possible Activities with an LLP

📈 Trading of Financial Instruments and Cryptocurrencies

An LLP can engage in trading stocks, bonds, ETFs, futures, options, and cryptocurrencies on regulated or decentralized markets.

If the activity is conducted by non-UK resident members and the LLP has no effective presence in the United Kingdom, no tax is due in the UK.

It is a perfect vehicle for managing personal portfolios, proprietary trading, arbitrage, DeFi, and strategies on centralized exchanges.

💼 Online Consulting (of Any Kind)

The LLP is an ideal structure for consulting activities, including:

Business consultancy

Personal and professional coaching

Holistic and energy-based consulting

Legal and tax advisory (where permitted)

IT, tech, software, and cybersecurity consulting

Any online-deliverable advisory service

All income can be managed efficiently, with limited liability and transparent taxation.

📦 Dropshipping, Online Commerce, Triangulation, Import/Export

An LLP can manage:

International dropshipping activities

Online sales of physical goods (via e-commerce)

Intra-EU or extra-EU commercial triangulation

Import/export with third-party customs handling

The LLP acts as an intermediary or seller, ensuring operational simplicity and tax efficiency.

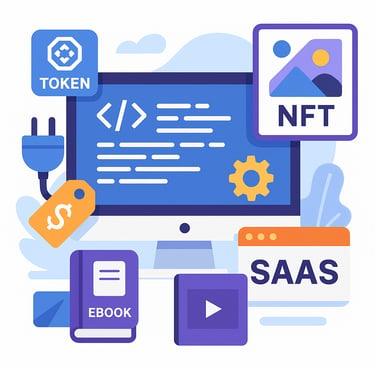

💻 Digital Product Sales and Software Development

Perfect for digital entrepreneurs:

Sales of software, plugins, templates, ebooks

SaaS (Software-as-a-Service) subscriptions

NFT, token, and blockchain project development or sales

Software development for third parties or internal use (e.g., proprietary trading systems, business tools)

📣 Digital Marketing and Online Creative Services

The LLP can provide any digital marketing or communication service, including:

Marketing agencies

Social media management

Influencer management

Web advertising / Google ADS / Meta ADS

Website and e-commerce development

App development

Photography, video editing, photo retouching

Branding, copywriting, and online campaigns

All services can be managed remotely, with clients anywhere in the world.

🛒 Online Sales (Physical and Digital Products)

The LLP can run platforms or stores for selling any type of product, physical or digital.

It can also be used to operate on marketplaces such as Amazon FBA, Etsy, eBay, Shopify, Gumroad, and others.

🤝 Commercial Intermediation with an LLP (B2B & B2C)

An LLP can act as an intermediary between companies, or between a company and the end customer, earning commissions on the sale of goods or services.

Perfect for brokerage, sales agents, referral partners, and online promoters, it is ideal for those who promote and sell third-party products or services via video calls, websites, or social media.

This model applies to both B2B (business-to-business) and B2C (business-to-consumer) activities, including dropshipping and digital services.

All operations can be carried out entirely online, without a physical office, with zero UK taxation if properly structured.

The LLP offers flexibility, tax efficiency, and limited liability—making it the ideal solution for independent sellers, agencies, or commercial startups.

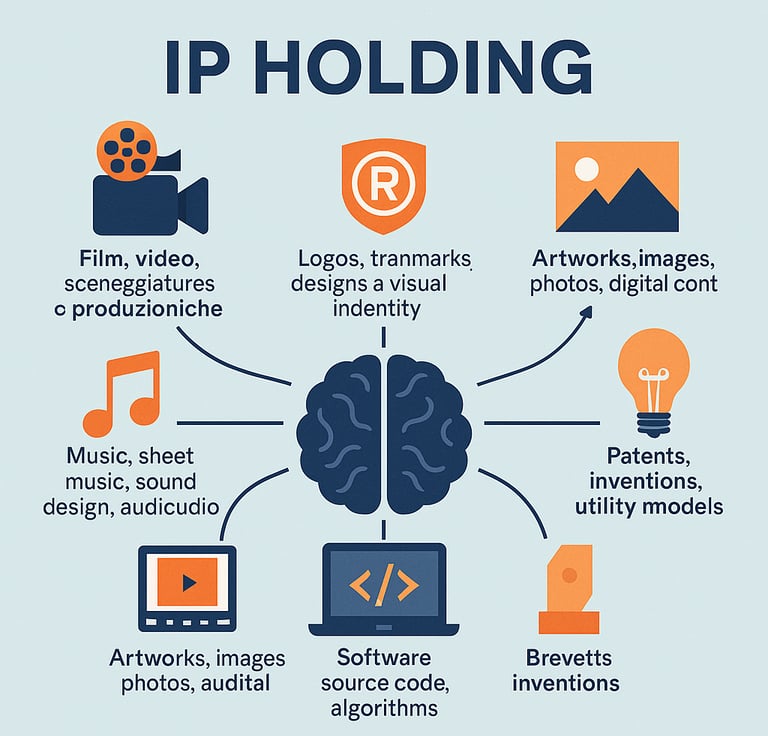

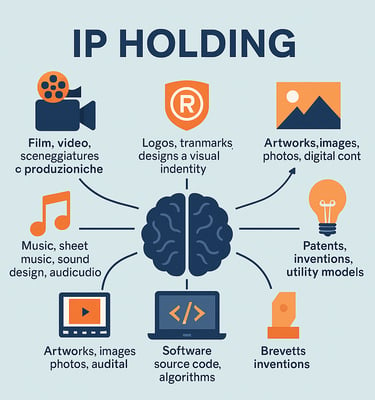

🛡️ Advantages of Using an LLP as an IP Holding Company

An LLP can be used as a holding company for intellectual property.

This structure is particularly beneficial for artists, creators, digital entrepreneurs, and production companies who wish to:

Protect their intangible assets (e.g., trademarks, copyrights, patents)

Centralize the management of rights and licensing

Receive royalty income with zero taxation (if properly structured)

It offers a secure, flexible, and tax-efficient vehicle for managing and monetizing intellectual property on a global scale.

VAT Registration Rules

🔍 VAT Requirement for a UK LLP: Everything You Need to Know

The need to register a VAT number for a UK-registered Limited Liability Partnership (LLP) depends solely on the nature and location of the business activity carried out.

Not all LLPs are required to have a VAT number in the UK.

✅ When a UK VAT Number Is Not Required

A UK LLP is not required to register for VAT in the United Kingdom if:

It does not have a permanent establishment or business activity in the UK (e.g., no offices, employees, warehouses, or operational base);

It does not sell goods or services to UK-resident customers;

Its UK-taxable turnover does not exceed £90,000 per year (current threshold set by HMRC).

In particular, there is no VAT obligation in the UK for LLPs engaged in international online activities such as:

Digital service sales

Software sales or online consulting

Trading (cryptocurrencies, forex, stocks)

Holding of assets or investments

🌍 Sale of Goods Within the European Union

If the LLP sells physical goods within the EU (for example, via e-commerce or distribution), but does not sell in the United Kingdom, there is no need for a UK VAT number.

In these cases, a VAT registration in an EU country, such as Ireland (IE), is sufficient and allows the LLP to:

Operate legally within the EU single market

Manage the import and export of goods

Use the intra-EU reverse charge mechanism

Register for the OSS scheme to handle B2C sales across Europe with a single VAT return

📄 VAT Registration: Obligations and Benefits

If you have a VAT number in the United Kingdom (GB/XI):

Obligations:

Submission of quarterly VAT returns to HMRC.

Benefits:

You can recover VAT paid on purchases made in the UK (e.g., software, services, supplies).

You gain greater tax credibility within the United Kingdom.

VAT registration is neither automatic nor mandatory for all LLPs—it depends on:

The economic presence in the United Kingdom

The type of activity (goods or services)

The location of customers and warehouses

📌 Our goal is to analyze your specific situation and determine whether—and where—it is advantageous to register for VAT, optimizing both your tax obligations and operational opportunities.

If you have a VAT number in Ireland (IE):

Obligations:

In Ireland as well, quarterly VAT returns are required.

Benefits:

You can take advantage of the intra-EU reverse charge mechanism:

No VAT is paid on purchases from EU suppliers with a VAT number.

No VAT is applied to sales made to EU customers who have a valid VAT number.

Access to the OSS (One-Stop Shop) scheme for centralized management of B2C sales across the EU.

🇬🇧 Sale of Goods in the United Kingdom

If the LLP sells goods within the UK, the situation changes:

VAT registration is recommended even below the threshold, to avoid issues related to audits and VAT refunds.

It becomes mandatory once the annual turnover from taxable activities in the UK exceeds £90,000.

🔐 Opening Costs

The initial cost of setting up an LLP primarily depends on the jurisdiction of the members, especially if offshore companies are involved.

The choice of jurisdiction affects:

Incorporation costs

Level of privacy

Banking accessibility

🌍 Recommended Jurisdictions for Offshore Members:

🇻🇬 BVI (British Virgin Islands)

A solid and well-recognized jurisdiction. However, the director’s name is publicly listed in official registries.

🇰🇾 Cayman Islands

Offers maximum confidentiality, though incorporation costs are higher compared to other options.

🇸🇨 Seychelles

A highly private and low-cost jurisdiction.

Bank account opening may be more complex, but with our support, it’s possible to obtain corporate bank or fintech accounts.

🇧🇸 Bahamas

Good privacy, well-known jurisdiction, suitable for international operations.

🇦🇮 Anguilla

Light structure, excellent anonymity, and low costs.

🇻🇨 Saint Vincent & the Grenadines

One of the most cost-effective options with strong privacy. However, bank account opening requires proper structuring and guidance.

⚙️ Annual Operating Costs

Annual costs depend on several key factors:

Presence of a VAT Number in the UK and/or Ireland (IE)

→ Requires financial statements, VAT returns, and specific compliance procedures.Type and Complexity of the Business

→ Simpler activities (e.g., IP holding, licensing) are less expensive than high-volume, transaction-heavy businesses.Transaction Volume

→ Higher volume = greater accounting workload.

📌 If the LLP has no active VAT number and engages in a simple business model, the costs can vary significantly and remain lower.

🌍 Offshore Company Costs Are Fixed and Predictable

Offshore companies used as LLP members incur standard, recurring costs, which depend on the jurisdiction of incorporation.

They typically include:

Fixed annual government fees

Registered agent renewal fees

✅ These are predictable and stable costs over time, with minimal fluctuations.

Opening Costs and Operating Costs

Contact Us

Do you have questions or need personalized advice?

We’re here to help you structure your business with tailor-made international tax solutions.

📞 Phone Contacts

🇬🇧 United Kingdom: +44 746 699 4615

📧 Email

info@onshorefreedom.com

💬 Direct Messaging

Prefer more private or immediate communication?

You can also reach us directly via:

Telegram: @onshorefreedom

WhatsApp: +44 746 699 4615

info@onshorefreedom.com

+44 74 66 99 46 15

Nantra LLP is the owner and manager of this website. As well as the logo and the brand OnShore Freedom and the domain name of the website ''onshorefreedom.com'' .

Nantra LLP © 2025. All rights reserved.

Nantra LLP, Company number NC001737,

Address: Unit 19 Antrim Enterprise Park, Greystone Road 58, Antrim, Northern Ireland, BT41 1JZ, United Kingdom.

UK VAT no: GB447880552 VIES VAT no: XI447880552

Freedom and financial indipendencefor your business.

Home NI LLP Tax Optimization Strategies UK Holding Jersey Trust Micro Businesses Services Who we are Contacts Privacy Policy Terms & Conditions